The past decade has been unprecedented in terms of financial policy.

Specifically, low-interest rates and central bank stimulus into economies around the globe starting from arguably the 1970s/80s (indisputably since 2008) to today have led to recent volatility in inflation and sharp increases in interest rates leading to bank collapses, increased business bankruptcies, and financial pressure on individuals.

What are the forces behind this? Or better yet, what tools do governments and central banks have to stimulate the economy?

In economics class, we were usually taught that there are two main levers a central bank has at its disposal to keep inflation at 2% and unemployment at acceptable levels. The FED (central bank of the US) controls the amount of money and credit in the economy by changing interest rates and by ‘printing’ money (quantitative easing).

I recommend you check out Ray Dalio’s posts on what has happened in the past and what is currently happening in regard to these two levers, global powers, and social stability.

So, the recent changes in the financial health of major economies can be attributed to the rising interest rates and lack of capital being injected (QT) by central banks into the economy.

This post is about the third lever the FED has at its disposal which is usually overlooked. Which? Changing the minimum reserve requirements for banks.

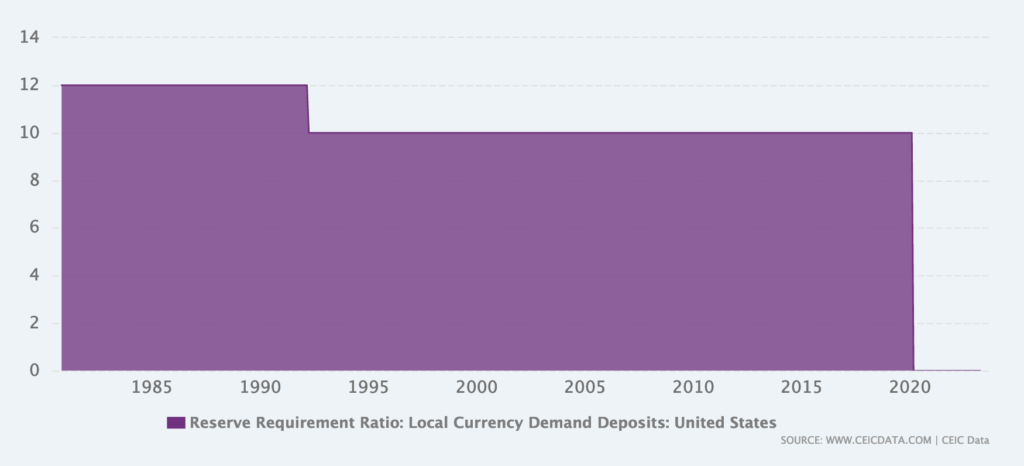

In simple terms, this is the amount of (liquid) assets a commercial bank needs to have on hand for every unit of deposits. For example, a 10% reserve requirement means that for every $10,000 in deposits, the bank is required to have $1000 in liquid assets for withdrawals.

Logically, one would assume that a higher reserve requirement would create a more stable bank (especially one that is less at risk of catastrophic bank runs) and lower reserve requirements lead to increased liquidity and thereby risk of a catastrophic bank run scenario.

Now, what is going to surprise a lot of readers is that the US has a reserve requirement of 0%. Yes, you read that right. Commercial banks do not need to hold any assets in reserves for the deposits they receive.

In the above graph, you see that this 0% capital reserve ratio is unprecedented. It was silently changed in 2020 and the only other country to have this unbalanced ratio is… Morocco! Though Europe is not far behind with 1%.

The media, FED, and financial institutions can claim that a self-sufficient or at the minimum healthier economy is just around the corner given higher rates and QT but with a FED balance sheet that is 80% bigger than pre-COVID levels AND a 0% reserve requirement, there is still a flood of liquidity swooshing through markets.

Over the past months, there have been serious writers and deep analyses unpacking the SVB and First Republic bank collapses. Many of the sound ones claim that the mark-to-market valuations of T-Bills in accounting systems (digression of short/long term assets and liabilities), the evolution to electronic withdrawal methods, and even the general system of using retail bank deposits towards trading with an intent to make a profit are the root causes of the collapses…

However, let’s realize that banks are aware of raising interest rates and are thereby taking risk management measures against this. They are also fully aware of QT. Matt Levine wrote that to solve this, commercial banks should not be allowed to speculate with retail deposits… this would mean that bank deposits would essentially be parked at the FED and any capital looking for a financial return would need to invest specifically in funds and vehicles where the return is higher but the risk is also clearly stipulated to the investors. This sounds great but is essentially raising the reserve ratio to 100%… which is clearly reducing risk but makes the financial system much more illiquid and inefficient (towards the capitalist goal of growth).

In an effort not to ramble in this post, I want to leave on this point: raising interest rates and QT are clearly part of the solution to restore an independent and healthy financial ecosystem BUT other parts of the puzzle also means restoring a balanced minimum reserve ratio to not over flood the economy with unnecessary liquidity.

Or do you believe that this is really the most balanced and fine-tuned financial system we are able to create in the 21st century?